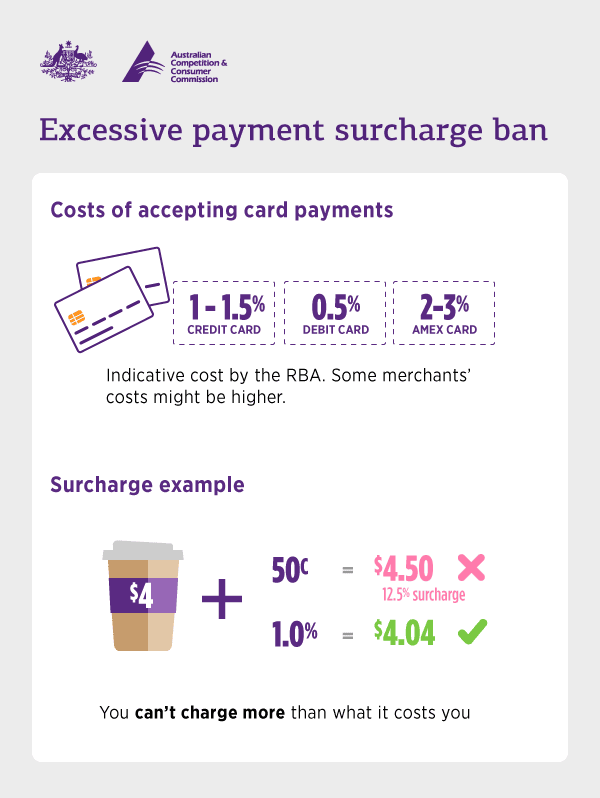

- Businesses can charge a surcharge for paying by card, but the surcharge must not be more than what it costs the business to use that payment type.

- If a business charges a payment surcharge, it must be able to prove the costs it is based on.

- If there is no way for a consumer to pay without paying a surcharge, the business must include the surcharge in the displayed price.

RBA Review Results: New Rules for Card Payments

On 31 March 2026, the Reserve Bank of Australia (RBA) released its final report into merchant card costs, its Conclusions Paper following the Review of Merchant Card Payment Costs and Surcharging. The Payments System Board concluded that a significant package of reforms is necessary to promote competition and efficiency in the Australian payments system.

What was decided?

- Removal of Surcharging: Surcharging will be removed on all debit, prepaid, and credit cards on the designated eftpos, Mastercard, and Visa networks.

- Lower Interchange Caps: The RBA will lower the caps on interchange fees paid by Australian businesses to help offset the removal of surcharge revenue.

- Increased Transparency: New rules will increase transparency over the fees charged by card networks and payment service providers, making it easier for businesses to compare costs.

- Implementation Date: Most of these changes, including the surcharging ban and domestic interchange reductions, will come into effect on 1 October 2026.

The ABA has reviewed the RBA’s Conclusions Paper and responded publicly to the reforms. Until 1 October 2026, the current surcharging guidelines (outlined below) remain in force.

Understanding the Current “Cost of Acceptance”

Current Surcharging Rules

Cost-Matching

The surcharge cannot be more than what it costs the business to use that specific payment type (like debit or credit).

Direct Costs Only

Fees can only cover the direct cost of the payment. Extra services, like point-of-sale software, cannot be added to a surcharge.

Proof of Cost

Businesses must be able to prove the costs they used to calculate their surcharge if they are asked to do so.

Ban on excessive payment surcharges

How much it costs a business to process a payment depends on the size of the business, the technology used, and the payment method.

This ban on excessive payment surcharges applies to:

- Visa

- MasterCard

- Eftpos

Generally the ban does not apply to other electronic payment methods. These include, but are not limited to:

- Buy now pay later (BNPL)

- PayPal

- Diners Club

- American Express

- taxi fares, whatever the payment type

Costs that businesses can include

The Reserve Bank of Australia sets out the costs that businesses can include when determining their reasonable costs of accepting payment types.

Before introducing a payment surcharge, businesses should read the ACCC’s Payment surcharges guide and the Reserve Bank of Australia guidance material. Consumers may also wish to read these guides for further information about how excessive payment surcharges are calculated.

The Reserve Bank of Australia has concluded its Review into Retail Payments Regulation, which examined the costs merchants face when accepting card payments and the framework for surcharging.

Frequently Asked Questions

Is the surcharging ban already in effect?

No. While the RBA has announced a ban on surcharging for Visa, Mastercard, and eftpos networks, the change is scheduled to come into effect on 1 October 2026. Until that date, current surcharging rules remain in place.

How much can a business currently charge as a surcharge?

Under current “Cost-Matching” rules, a business cannot charge more than what it costs them to process that specific payment type. For example, if it costs a business 1% to accept a credit card, the surcharge cannot exceed 1%.

Does the ban apply to American Express or PayPal?

The proposed ban specifically applies to the eftpos, Mastercard, and Visa networks. It generally does not apply to other electronic payment methods like American Express, Diners Club, PayPal, or Buy Now Pay Later (BNPL) services.

What should I do if I think a surcharge is excessive?

If you believe a business is charging an excessive payment surcharge, you can report it to the Australian Competition and Consumer Commission (ACCC). Businesses are required to be able to prove their cost of acceptance if challenged.

Why do banks support the surcharging ban?

The ABA supports the ban to provide consumers with price certainty at the checkout. We believe Australians deserve to know that the price shown on the shelf is the final price they will pay, whether paying in-store or online.