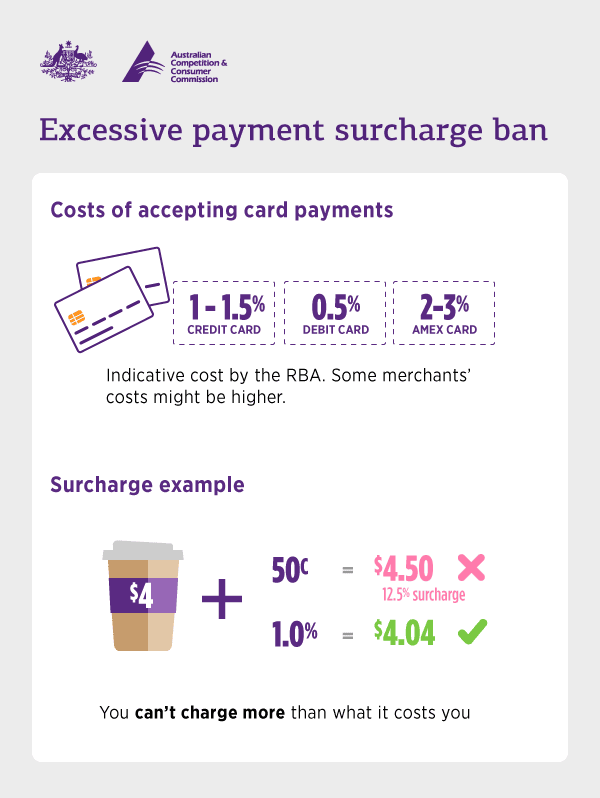

- Businesses can charge a surcharge for paying by card, but the surcharge must not be more than what it costs the business to use that payment type.

- If a business charges a payment surcharge, it must be able to prove the costs it is based on.

- If there is no way for a consumer to pay without paying a surcharge, the business must include the surcharge in the displayed price.

Update: RBA Review of Card Payments

The Reserve Bank of Australia (RBA) is currently finalising a review into the costs of card payments. A final report is expected this Tuesday, 31 March, which is likely to change how surcharging works for Australian businesses and shoppers.

What is being looked at?

- A ban on debit card surcharges: So the price you see on the shelf is the price you pay at the checkout.

- Lower fees for businesses: Reducing the wholesale costs banks pay to help shops and small businesses cover the cost of card payments.

- More transparency: Making it easier for small businesses to see exactly what they are being charged for each transaction.

The ABA is following this review closely. Until new rules are announced, the current surcharging guidelines (outlined below) still apply.

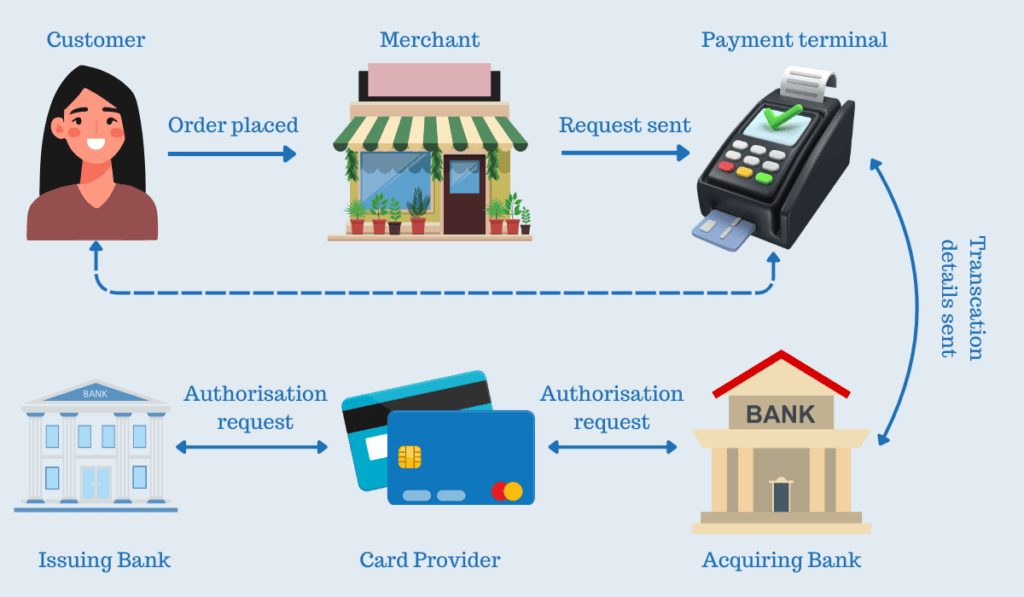

How does surcharging work?

Surcharging is a practice where businesses pass on the cost of processing certain electronic payments. All forms of payment, including the use of cash, incur costs to the business. However regulation, allows for debt and credit cards to be surcharged.

In Australia, there are specific rules and regulations that businesses must follow when applying surcharges. The surcharge must not exceed the actual cost of processing the payment. This means that businesses can only include costs directly related to accepting that particular payment method.

Businesses must also be able to prove the costs they used to calculate the surcharge. This ensures transparency and helps prevent excessive surcharging, which is illegal and can lead to significant fines and reputational damage. The Reserve Bank of Australia (RBA) and the Australian Competition and Consumer Commission (ACCC) provide guidelines and resources to help businesses comply with these regulations.

Current Surcharging Rules

Cost-Matching

The surcharge cannot be more than what it costs the business to use that specific payment type (like debit or credit).

Direct Costs Only

Fees can only cover the direct cost of the payment. Extra services, like point-of-sale software, cannot be added to a surcharge.

Proof of Cost

Businesses must be able to prove the costs they used to calculate their surcharge if they are asked to do so.

Ban on excessive payment surcharges

How much it costs a business to process a payment depends on the size of the business, the technology used, and the payment method.

This ban on excessive payment surcharges applies to:

- Visa

- MasterCard

- Eftpos

Generally the ban does not apply to other electronic payment methods. These include, but are not limited to:

- Buy now pay later (BNPL)

- PayPal

- Diners Club

- American Express

- taxi fares, whatever the payment type

Costs that businesses can include

The Reserve Bank of Australia sets out the costs that businesses can include when determining their reasonable costs of accepting payment types.

Before introducing a payment surcharge, businesses should read the ACCC’s Payment surcharges guide and the Reserve Bank of Australia guidance material. Consumers may also wish to read these guides for further information about how excessive payment surcharges are calculated.